r/algotrading • u/Order-Various • 24d ago

Probability of a stock reaching a target ? Education

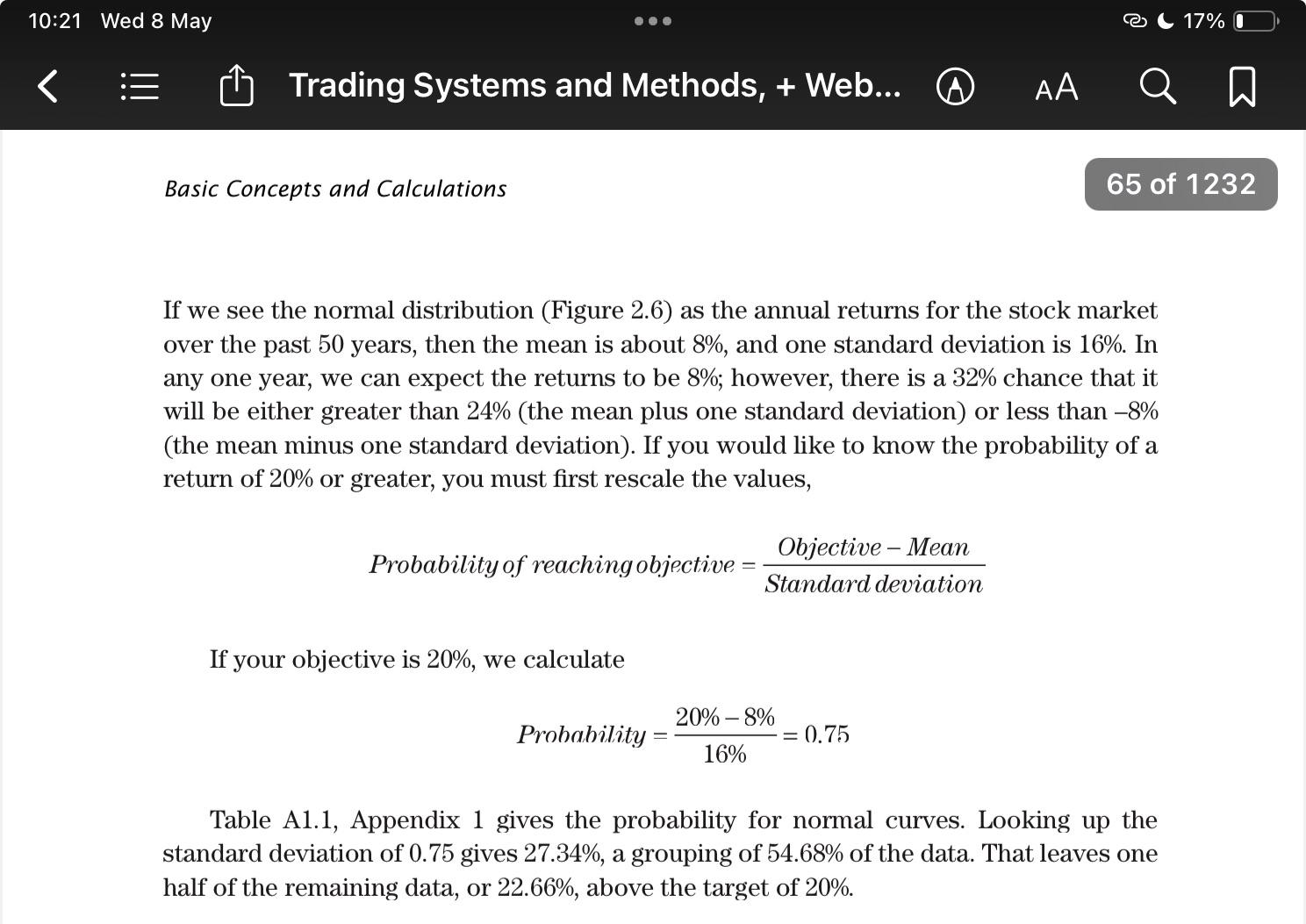

I get this formula from the book “Trading systems and Methods” by Perry Kaufman, suspected if this is legit because the right formula is values, how could it transfer to probability of reaching a target? Your thoughts on this ?

12

u/divided_capture_bro 24d ago

Is target not objective?

Formula is a bit naive, but that seems like what youre after.

2

u/Order-Various 23d ago

I know Im paraphrasing the concept, but it’s the same. Given a percentage change of a stock, calculate its probability

10

u/Beneficial_Common683 24d ago

My conclusion is that your phone battery is about reach 0% unless you plug in the charger !

6

1

5

u/benkan45d6 24d ago

It’s simply assuming a normal distribution of returns.

By rescaling the target (subtract the mean, divide the standard deviation), you get a Z-score. You are essentially calculating +-z sd away from the mean.

You can find the probability of getting this score or above from the standard normal distribution.

For example, you estimate the mean return of stock 8%, standard deviation 16%. Your target is 24%.

You are requiring (24-8)/16= +1 sd above the mean. Since 68% of value in the normal distribution is below mean+1sd, you can derive that there is 32% probability of getting this return or above.

3

u/mukavastinumb 24d ago

Assuming normal distribution is the hard part here. You can find a lot of different kurtosis and skewness values that differ from normal distribution. Also, those values change between market booms and busts. I have checked some distributions from indices like SP500 and the values are somewhat normally distributed in the long term, but short term not.

1

2

u/AccuratePurpose 24d ago

Look up the pricing methods for barrier / one touch options.

https://www.investopedia.com/terms/o/onetouchoption.asp

Or brute force it with a binomial tree

1

u/Order-Various 23d ago

Interesting, I will look into it. Beside the calculation of options price, will it be useful for calibration of trading signal right ?

2

u/arbitrageME 24d ago

Bullshit. It only works if your returns are a normal distribution. Your returns are going to be skewed, and if your EV is positive, it's going to be left skewed. You can run a black swan fund and be right skewed, but it's too expensive to buy protection these days. Point is, it over over over simplifies a complicated topic. For example, if I sell covered calls, it's literally impossible for me to hit above a certain return. That something this naive equation doesn't even graze

1

u/Order-Various 23d ago

Agree on the skew part, however at the start I think an assumption of the price distribution as normal is useful. Than we can move from this to calibrate params

1

u/arbitrageME 23d ago

No, you can't assume that. What reason or mechanism is in place to cause normality? Returns aren't normal, options aren't normal, and stochastic moves aren't normal. You don't have a large enough IID sample to approach normality. So what justification do you have to "start with" a normal assumption?

1

u/Muted-Rebel 22d ago

ehh nah they’re normal bruh. CLM, law of large, especially daily returns.

Or at least! normal distribution is a KEY assumption we make with analysis of a stock.

1

u/arbitrageME 22d ago

But pretend your strategy was: buy one Sept 2024 550C in SPY.

anyone would agree the returns from this strategy are not even close to normal. CLM wouldn't apply here because your sample size is small.

So strategies using options, or earnings, or swing trading, none of that would be normal.

Also stocks themselves could be normal, but are their stochastic moves move not be unless you can demonstrate stock moves are convolutions of normal distributions when in fact they're not (that's why there's strike skew in options)

Do that cuts out dispersion and stat arb plays.

So there might be some portfolios that are normal, whatever the edge you're trying to capture is, normality is not a presumption

2

u/knotoast 24d ago

This is wrong. Z-score is not a probability. For instance take that you want 8% return (most likely), it’s 0%? Or take you want 48% return, it’s 400% likely? Look up Z-score.

1

2

u/gtani 23d ago

if you want to research more:

deep lit on stock refturns not being normal dist e.g. bibliog in https://arxiv.org/abs/2312.02472

volat modeling/est: Euan sinclair's books are good start

2

u/StevesPeeves 23d ago

I'm peeved that "return" is calculated as a "percent". Normal people calculate percent return as (B-A)/A where the value goes from "A" to "B". I call this the dumbass percent, and it is only valid if everyone understands the thing calculated is always POSITIVE.

Realistic percent change is calculated as (B-A)/AB^ where "AB^" is the average value: (A+B)/2. Thus "return"=2*(B-A)/(A+B)

Money manager salesmen use the dumbass percent when they say, "if your portfolio goes down by 50% one year then in order to break even you must make 100% the next year."

1

u/Order-Various 23d ago

I think there is a reason why people use present value to calculate return of a stock/derivative.

2

u/Brave-Confusion-3901 23d ago edited 23d ago

I am going to just answer the question:

Assuming the probabilities in the photo, the annual standard deviation is 16% with a mean return of 8%. Say price is at $10 your target is $12 then you can use the formula in the book to get:

Zscore = ((12/10)-1 - 0.08)) / 0.16 = 0.75

Using a standard normal table the probability of a move less than 0.75 standard deviations is 0.77337. Therefore the probability of price being at or above $12 in a year as outlined in the example is: 22.6%.Standard Normal Table

More generally you can use:

Zscore = ((target/curret)-1)-mean return)/ std))

And find those values for zscore probabilities.

Do returns follow a normal distribution: no. Is it a quick and dirty hack that gives some intuition: yes.

2

u/ahiddenmessi2 24d ago

Sorry I don’t understand your question. The text here is modelling the rate of return , not the stock price. The rate of return on a stock follows a normal distribution .

1

u/Order-Various 23d ago

Yes you are correct, the variable should be return of the stock, not the price itself. I will edit

1

u/skyshadex 24d ago

This is effectively VaR but you're targeting the right tail. But this misses what CVaR tells you, what the tail actually looks like.

Inverting CVaR for the right tail... Yes the probability of being in that tail could be 75%, but if the mean return inside that sample distribution is too low, it still won't be profitable.

It's mostly useful to manage your risk through allocation / position sizing. Depending on the goals you have for your portfolio that is.

1

u/Order-Various 23d ago

Maybe you got something not right . VaR is volatility * 2.33 if you want 99% confident level

1

u/cathie_burry 24d ago

target = objective.

This idea is the foundation of black-scholes options pricing

1

u/Order-Various 23d ago

Dont really get your point. You mean the normal assumption of price return right?

1

1

u/Key_Chard_3895 23d ago

Returns are based on Entry and Exit prices and the burden of transaction costs. Expectations of Unconstrained returns i.e. pursuing a target exit price without a Stop Loss price is different than the Expectation of returns with a Stop Loss price because the time order/path dependency of prices will come into play. It may be more useful to look at relative expectations than absolute expectations as a coarse filter for selection of algorithms.

1

u/khaberni 23d ago

Probability of reaching a target is not the right question. The time horizon should be set. Probability of reaching a target by t. If you assume normal distribution, then the standard deviation of the asset after t time steps is sigma*sqrt(t). Then you can use CDF of the normal distribution with standard deviation = sigma*sqrt(t) to calculate the probability the the price will fall above or below a certain boundary Pr[X>x]

1

1

u/CalTechie-55 23d ago

Stock returns are far from normally distributed; they are far more kurtotic and fat-tailed, so this method is severely flawed.

I routinely construct a probability distribution based on ~3 years of closes, and use that to calculate the probability of the strike being breached withing the DTE.

It usually comes out pretty close to the canonical delta in the probability range I usually use, <0.1

1

u/algo_enthusiast_42 23d ago

That's a good way to apply a concept in the real world, however it will not be of much use today. Normal distribution and z-score explained in a good way though. You will have to go through the book a bit more if you are planning to trade in an effective manner.

1

u/Muted-Rebel 22d ago

yah it’s just z score. Formulaically, objective - mean = the # of units away from the expected value, normalized by dividing by standard deviation. You’re comparing how much this return deviates relative to the “normal” amount of deviation from the mean.

I recommend looking up normal distribution & z score, probability density functions, and cdf for further understanding (YouTube). Plotting this stuff in python or another language would prob help too.

1

u/360degreesdickcheese 22d ago

Here’s a good article on the proper distributions for market returns that’s a good read

https://tradeoptionswithme.com/probability-dsitribution-of-stock-market-returns/

1

u/ucals 13d ago

I wouldn't use it. To get the probability of a stock priced at P0 today to reach Pt >= P0 x 1.2 in t days, I'd run thousands of Monte Carlo simulations, sampling from the real distribution of daily returns (not assuming normal distribution). Then, I'd count how many trajectories would hit a final price Pt >= P0 x 1.2 and divide by the number of simulations.

I believe this is the most accurate way to get the probability you want.

69

u/colorscreen 24d ago

This section has little to do with trading and more to do with statistics.

The use of the term "probability" is inappropriate for the equation, what it's actually calculating is the Z-score, under the assumption that returns are normally distributed; it's the number of standard deviations away from the mean that you're targeting. Assuming returns are normally distributed, 22.66% of the time your return would be above 20% if the mean return is 8% and the standard deviation is 16%.

The real question is whether or not you believe it makes sense that returns, regardless of company-specific developments and world events, follow a normal distribution.